Related Tool:

What is an Interest-Only Loan?

An interest-only loan is exactly what it sounds like: a loan structure where for a specified initial period, you only pay interest on the amount you’ve borrowed, not the principal. This setup means less payments in the loan’s early years. Though it also means you can’t reduce the loan balance until the interest-only period ends.

Suppose you borrow $200,000 at an annual interest rate of 5%. If your loan allows for 5 years of interest-only payments, you’ll only have to pay the interest on the $200,000 during that time, nothing toward the actual balance. When the interest-only term ends, your payments increase significantly because you’ll need to repay both the principal and interest throughout the remaining loan period.

This metric is common in real estate investments and jumbo mortgages, but can also be used by anyone who needs lower upfront payments, whether it’s to manage cash flow or fund renovations during a construction loan.

How This Interest-Only Loan Calculator Works

Our tool to calculate interest-only loan is built to give you a full breakdown of your loan’s payment structure from interest-only installments to what happens once principal repayment begins, along with a detailed graphical chart and yearly & monthly amortization tables. Here’s how it functions:

Inputs You Provide:

- Loan Amount – How much you’re borrowing.

- Annual Interest Rate (%) – The yearly cost of borrowing.

- Interest-Only Period (Years) – The number of years you’ll pay interest-only.

- Total Loan Term (Years) – The complete lifespan of the loan.

- Payment Frequency – Choose periods between monthly, quarterly, or annually.

Outputs You Get:

After entering these details, the interest-only payment calculator will provide:

- Interest-Only Payment Amount

- Principal + Interest Payment After IO Period

- Payment Increase When IO Period Ends

- Total Interest Paid During IO Period

- Total Interest Over Full Loan Term

- Total Amount Paid by Loan End

How to Calculate Interest-Only Loan (Payments)

During the interest-only phase, the formula is simple:

For example, if you borrow $300,000 at 6% annual interest and choose monthly payments:

- Monthly Rate = 6% ÷ 12 = 0.5%

- Interest-Only Payment = $300,000 × 0.005 = $1,500 per month

You only cover the interest cost, so the loan balance stays the same.

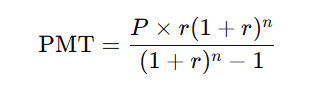

Once the interest-only phase wraps up, the scenario changes. Now you must repay the original loan over the remaining loan term along with interest. To calculate the new, higher payment (also called the fully amortized payment), the calculator uses this formula:

Where:

- P is the loan amount,

- r is the periodic interest rate,

- n is the number of remaining payment periods.

For example, if you had a $300,000 loan, a 6% annual rate, a 5-year interest-only period, and a total loan term of 30 years:

- Remaining loan period = 25 years = 300 months

- Monthly payment = about $1,933.28 after the 5 years

It’s a big increase from your initial $1,500 monthly interest-only payment.

Let’s walk through a full example – Imagine the scenario involving these given values:

- Loan Amount: $250,000

- Interest Rate: 5% annually

- Interest-Only Period: 10 years

- Total Loan Term: 30 years

- Payment Frequency: Monthly

Our interest-only loan/payment calculator would return this output with detailed visual chart and long amortization table:

- Interest-Only Payment: $1,041.67 per month

- Principal + Interest Payment (after 10 years): $1,639.18

- Payment Increase: $597.51

- Total Interest (Interest-Only Phase): $125,000

- Total Interest (Entire Loan): $264,104.48

- Total Paid Over 30 Years: $514,104.48

So you can see how much less payments at start means a much higher cost in the long run if you’re not aggressively managing your loan or planning to refinance.

How Payment Frequency Affects Interest

Our tool allows you to change how often payments are made. Here’s how frequency shifts the numbers:

- Monthly – 12 payments per year (most common)

- Quarterly – 4 payments per year

- Annually – 1 payment per year

Interest is divided by the number of payments per year, so quarterly or annual payments mean fewer but bigger payments. They also result in slightly more interest over time because the loan balance is unpaid for long stretches.

Example:

Let’s say you borrow $100,000 at 6% annually for 5 years of interest-only:

- Monthly IO Payment: $500

- Quarterly IO Payment: $1,500

- Annual IO Payment: $6,000

While the totals during the interest-only phase may look the same at first glance, compounding and timing nuances make monthly payments slightly more cost-effective overall.

The Use of Interest-Only Loan

Interest-only loan is not widely used in the finance market, but it’s important in many scenarios where required:

- Real Estate Investors: Lower payments at first = higher cash flow potential.

- Homebuyers Expecting Increased Income: Useful if you expect a financial jump (e.g., residency-to-doctor or grad school-to-career).

- Construction Projects: Avoid paying principal before the asset generates income.

- Short-Term Use: Planning to refinance or sell the property before the interest-only period ends.

However, you need to plan wisely; the shift from low to high amounts can catch borrowers off guard. Our calculator helps you see that increase before signing anything.

Total Interest Paid

A common mistake is assuming low monthly payments mean a cheap loan but that’s not true. In fact, total interest paid on an interest-only loan can be much higher than a usual loan over the same term.

This calculator shows both:

- Interest during the interest-only period, and

- Total interest across the entire loan

This way, you get a full picture of what your loan is actually costing you, which helps you decide if the early flexibility is worth the long-term tradeoff.

Usama, Ali "Interest Only Loan Calculator" at https://zeecalculator.com/interest-only-loan-calculator from ZeeCalculator, https://zeecalculator.com - Online Calculators